6. Factors of Production: The Law of Returns

6. Factors of Production: The Law of ReturnsWe have concluded that the value of each unit of any good is equal to its marginal utility at any point in time, and that this value is determined by the relation between the actor’s scale of wants and the stock of goods available. We know that there are two types of goods: consumers’ goods, which directly serve human wants, and producers’ goods, which aid in the process of production eventually to produce consumers’ goods. It is clear that the utility of a consumers’ good is the end directly served. The utility of a producers’ good is its contribution in producing consumers’ goods. With value imputed backward from ends to consumers’ goods through the various orders of producers’ goods, the utility of any producers’ good is its contribution to its product—the lower-stage producers’ good or the consumers’ good.

As has been discussed above, the very fact of the necessity of producing consumers’ goods implies a scarcity of factors of production. If factors of production at each stage were not scarce, then there would be unlimited quantities available of factors of the next lower stage. Similarly, it was concluded that at each stage of production, the product must be produced by more than one scarce higher-order factor of production. If only one factor were necessary for the process, then the process itself would not be necessary, and consumers’ goods would be available in unlimited abundance. Thus, at each stage of production, the produced goods must have been produced with the aid of more than one factor. These factors co-operate in the production process and are termed complementary factors.

Factors of production are available as units of a homogeneous supply, just as are consumers’ goods. On what principles will an actor evaluate a unit of a factor of production? He will evaluate a unit of supply on the basis of the least importantly valued product which he would have to forgo were he deprived of the unit factor. In other words, he will evaluate each unit of a factor as equal to the satisfactions provided by its marginal unit—in this case, the utility of its marginal product. The marginal product is the product forgone by a loss of the marginal unit, and its value is determined either by its marginal product in the next stage of production, or, if it is a consumers’ good, by the utility of the end it satisfies. Thus, the value assigned to a unit of a factor of production is equal to the value of its marginal product, or its marginal productivity.

Since man wishes to satisfy as many of his ends as possible, and in the shortest possible time (see above), it follows that he will strive for the maximum product from given units of factors at each stage of production. As long as the goods are composed of homogeneous units, their quantity can be measured in terms of these units, and the actor can know when they are in greater or lesser supply. Thus, whereas value and utility cannot be measured or subject to addition, subtraction, etc., quantities of homogeneous units of a supply can be measured. A man knows how many horses or cows he has, and he knows that four horses are twice the quantity of two horses.

Assume that a product P (which can be a producers’ good or a consumers’ good) is produced by three complementary factors, X, Y, and Z. These are all higher-order producers’ goods. Since supplies of goods are quantitatively definable, and since in nature quantitative causes lead to quantitatively observable effects, we are always in a position to say that: a quantities of X, combined with b quantities of Y, and c quantities of Z, lead to p quantities of the product P.

Now let us assume that we hold the quantitative amounts b and c unchanged. The amounts a and therefore p are free to vary. The value of a yielding the maximum p/a, i.e., the maximum average return of product to the factor, is called the optimum amount of X. The law of returns states that with the quantity of complementary factors held constant, there always exists some optimum amount of the varying factor. As the amount of the varying factor decreases or increases from the optimum, p/a, the average unit product declines. The quantitative extent of that decline depends on the concrete conditions of each case. As the supply of the varying factor increases, just below this optimum, the average return of product to the varying factor is increasing; after the optimum it is decreasing. These may be called states of increasing returns and decreasing returns to the factor, with the maximum return at the optimum point.

The law that such an optimum must exist can be proved by contemplating the implications of the contrary. If there were no optimum, the average product would increase indefinitely as the quantity of the factor X increased. (It could not increase indefinitely as the quantity decreases, since the product will be zero when the quantity of the factor is zero.) But if p/a can always be increased merely by increasing a, this means that any desired quantity of P could be secured by merely increasing the supply of X. This would mean that the proportionate supply of factors Y and Z can be ever so small; any decrease in their supply can always be compensated to increase production by increasing the supply of X. This would signify that factor X is perfectly substitutable for factors Y and Z and that the scarcity of the latter factors would not be a matter of concern to the actor so long as factor X was available in abundance. But a lack of concern for their scarcity means that Y and Z would no longer be scarce factors. Only one scarce factor, X, would remain. But we have seen that there must be more than one factor at each stage of production. Accordingly, the very existence of various factors of production implies that the average return of product to each factor must have some maximum, or optimum, value.

In some cases, the optimum amount of a factor may be the only amount that can effectively co-operate in the production process. Thus, by a known chemical formula, it may require precisely two parts of hydrogen and one part of oxygen to produce one unit of water. If the supply of oxygen is fixed at one unit, then any supply of hydrogen under two parts will produce no product at all, and all parts beyond two of hydrogen will be quite useless. Not only will the combination of two hydrogen and one oxygen be the optimum combination, but it will be the only amount of hydrogen that will be at all useful in the production process.

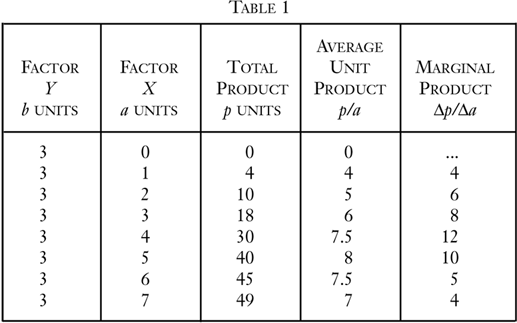

The relationship between average product and marginal product to a varying factor may be seen in the hypothetical example illustrated in Table 1. Here is a hypothetical picture of the returns to a varying factor, with other factors fixed. The average unit product increases until it reaches a peak of eight at five units of X. This is the optimum point for the varying factor. The marginal product is the increase in total product provided by the marginal unit. At any given supply of units of factor X, a loss of one unit will entail a loss of total product equal to the marginal product.

Thus, if the supply of X is increased from three units to four units, total product is increased from 18 to 30 units, and this increase is the marginal product of X with a supply of four units. Similarly, if the supply is cut from four units to three units, the total product must be cut from 30 to 18 units, and thus the marginal product is 12.

It is evident that the amount of X that will yield the optimum of average product is not necessarily the amount that maximizes the marginal product of the factor. Often the marginal product reaches its peak before the average product. The relationship that always holds mathematically between the average and the marginal product of a factor is that as the average product increases (increasing returns), the marginal product is greater than the average product. Conversely, as the average product declines (diminishing returns), the marginal product is less than the average product.25

It follows that when the average product is at a maximum, it equals the marginal product.

It is clear that, with one varying factor, it is easy for the actor to set the proportion of factors to yield the optimum return for the factor. But how can the actor set an optimum combination of factors if all of them can be varied in their supply? If one combination of quantities of X, Y, and Z yields an optimum return for X, and another combination yields an optimum return for Y, etc., how is the actor to determine which combination to choose? Since he cannot quantitatively compare units of X with units of Y or Z, how can he determine the optimum proportion of factors? This is a fundamental problem for human action, and its methods of solution will be treated in subsequent chapters.

- 25For algebraic proof, see George J. Stigler, The Theory of Price (New York: Macmillan & Co., 1946), pp. 44–45.