The go-to bullish indicators highlighted by pundits these days are the high levels of sidelined mutual fund cash and the AAII investor sentiment survey hitting its highest bearish reading since 2009:

Traditionally, these signals suggest that most of the carnage is priced into markets, indicating that it might be time to buy. However, these data sets only illustrate ACTIVE investor sentiment. Given that passive funds, by definition, do not strategically manage their cash levels nor do index fund patrons pay $40 per year to participate in the AAII survey, these figures give us little insight into the passive investing world. In stark contrast, Vanguard has reported net inflows to their passive vehicles of $400 million for the month of March (i.e. one behemoth is still buying). More evidence that passive investors remain all-in can be found in the lack of redemptions world-wide:

While the markets have seen considerable selling in certain sectors as active managers have rebalanced their weightings, capital is not being withdrawn from markets at any meaningful scale. These are strategic moves by fund managers, not necessity-driven liquidations. If they were, one could expect them to originate from two places: low-income earners paying their bills and/or margin calls.

Considering most active wealth managers require a minimum investment of $50,000 while an index fund account with BlackRock only requires $1,000, it’s easy to see why low-to-middle-income earners opt for a passive plan. These investors add up, with total passive assets having overtaken active’s share in the $11.6 trillion US equity funds market, “driven largely by the growth of funds tracking the S&P 500”, according to Bloomberg (i.e. the S&P may be hit hardest in a true recession).

As the cost of living continues to rise and monetary tightening leads to higher mortgages, credit card APRs, and layoffs as zombie companies scramble to service their increasingly costly debt, it will be the low-income-index-fund-buyers who initiate mass redemptions out of necessity to fund their daily lives. This will flip the Big Three passive funds (or the “Giant Robot” as legendary short-seller Bill Fleckenstein refers to them) from bid to ask.

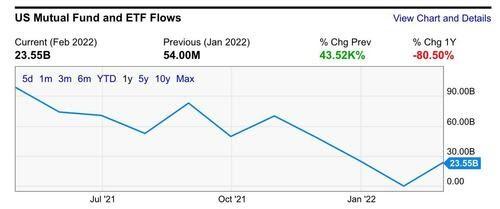

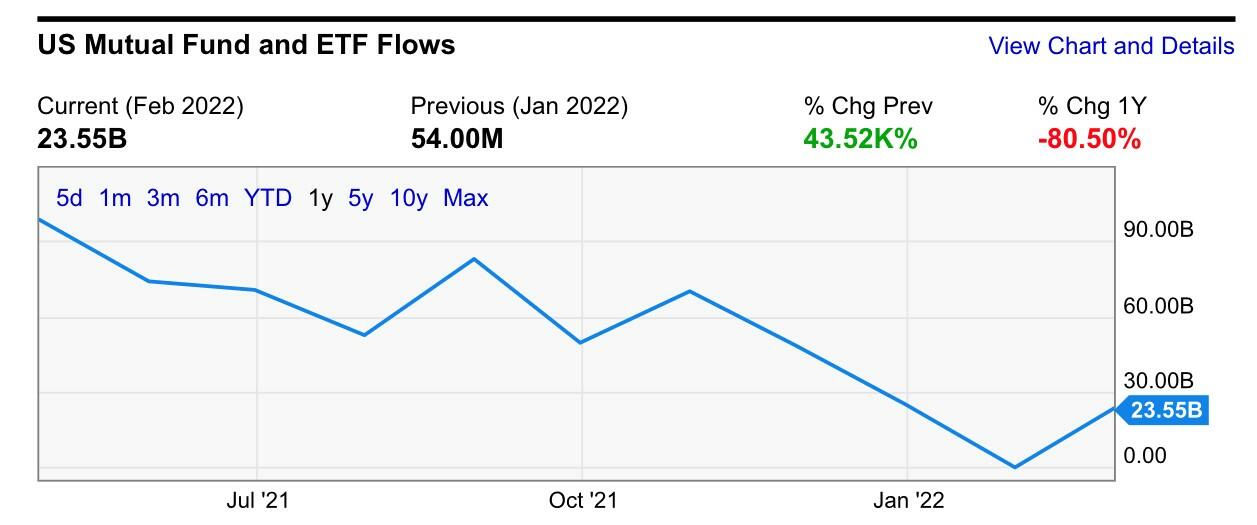

Passive capital flows dangerously close to negative territory (not including April which is beginning to see negative flows).

Those familiar with the work of Simplify Asset’s Michael Green into the effects of passive investing on equity markets will know: The Big Three are non-discretionary. When cash is flowing in, they hit buy. When it’s flowing out, they hit sell. Green believes passive’s distortions contribute to the more volatile price swings that have occurred during market downturns in recent decades.

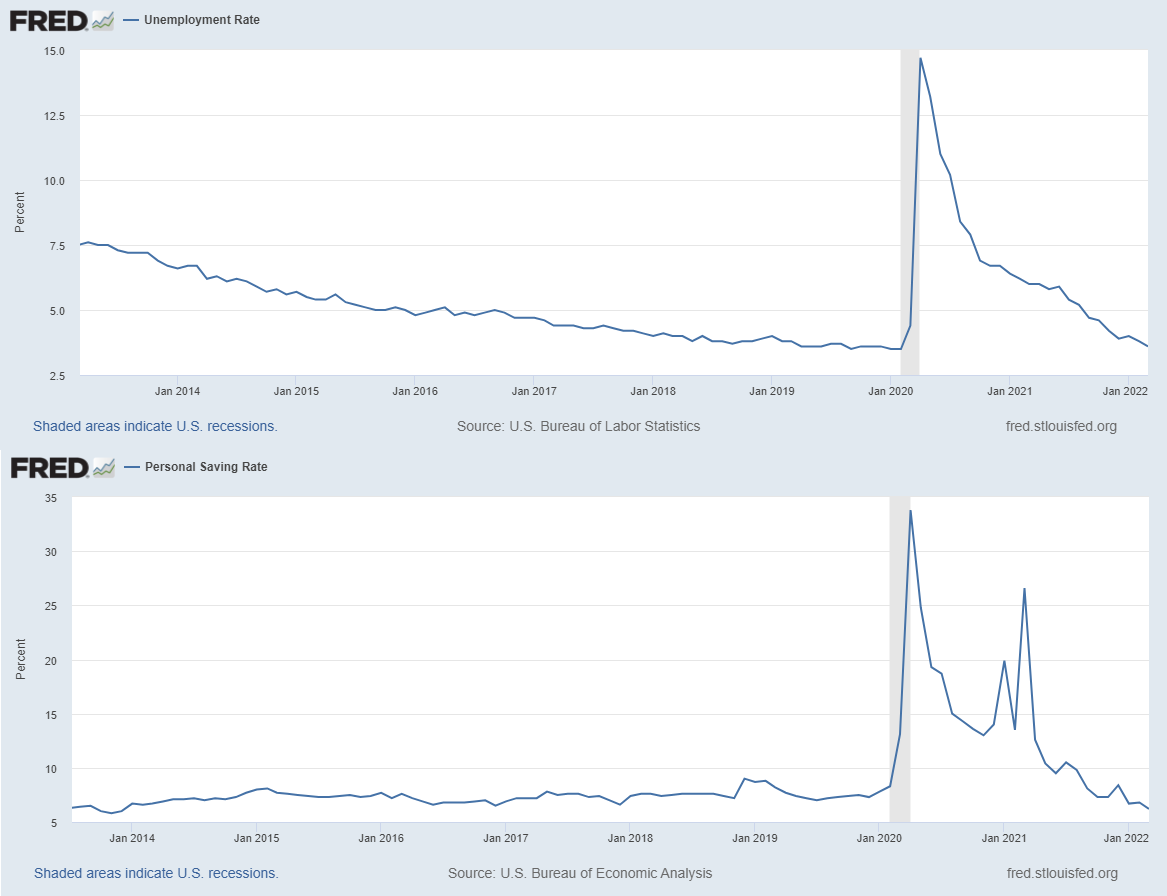

He provided me with a research paper claiming the rise of passive has created “substantially more inelastic aggregate demand curves for individual stocks,” meaning equity prices have become more sensitive to relatively smaller shifts in demand. This, combined with the jarring reversal of the most accommodative monetary policy the world has ever seen, could result in devastation for markets. And the data indicate these behemoths are just barely waking up. With unemployment that can’t go much lower and ominously depleting levels of personal savings, this is a powder keg set to blow:

A few bonus thoughts: consider the now commonplace compensation trend by which executives of public companies are paid in stock that they then borrow against to fund expenditures. At what price level will we see executive-level margin calls and mass selling by the .001%-ers? This could be why many individual names are already down 70-80%.

It seems there are several phenomena that have acted as market boons in the past decade or so, which are now primed to reverse. Still, I suspect active managers will be “buying the dip” in the coming weeks (as Warren Buffet just did), and this ironically may give the Fed more confidence in tightening.

{kind=link}

{kind=link}