Last week the FOMC announced that it would continue unchanged its policies of open-ended quantitative easing to the tune of $85 billion per month and targeting a zero interest rate for as long as the unemployment rate remains above 6.5 percent and (CPI) inflation does not exceed 2.5 percent. The FOMC polices should thrill Scott Sumner, a leader of the relatively new school of macro policy known as “market monetarism” and ranked 15th jointly with Fed Chairman Bernanke by Foreign Policy magazine on its list of 100 top global thinkers in 2012.

Market monetarism has experienced an amazingly rapid ascent in the past two years, especially in the blogonomics sphere and among economists toiling at small teaching colleges. Sumner and his fellow market monetarists advise the Fed to target nominal GDP, that is aggregate demand or total spending on goods and services in the economy. Briefly, they argue that because velocity is unpredictable, the Fed should manipulate the money supply so as to offset fluctuations in velocity and maintain a fixed rate of growth in the level of aggregate demand. Successfully doing so, they maintain, would considerably mitigate demand-side macroeconomic fluctuations.

Sumner was interviewed by Bloomberg columnist Caroline Baum the week prior to the latest FOMC meeting. Referring to the policy announced after the December FOMC meeting, Sumner characterized the Fed’s commitment to a zero interest-rate target as “a backdoor way of nominal GDP level targeting. The Fed would like a catch-up in growth before it starts tightening.” In other words, the Fed was implementing the Sumnerite market monetarist policy, even if it has gone far beyond reflating nominal GDP to its level at the peak of the bubble. Well, let’s see what that looks like.

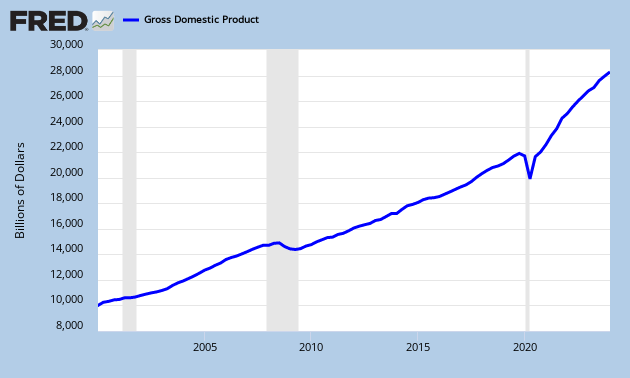

The chart shows that nominal GDP has been inflated to $15.829 trillion, almost 10 percent above its bubble peak of $14.416 trillion in early 2008. What kind of “catch-up” is this? Well for Sumner et al., in normal times the Fed should target a 3-5 percent increase in the level of nominal GDP. Since early 2010, nominal GDP has been growing at a rate slightly above 4 percent. During the high bubble years of 2003-2006, the growth rate was around 6.5 percent. Yet, despite target growth, the recent run-up in nominal GDP has gone hand-in-hand with massive price inflation in asset and commodity markets. As economist Mark Thornton has recently shown nascent bubbles are forming throughout the economy. The producer price index for commodities has hit record levels. The gold price has set new records and is fluctuating between 60 and 80 percent above its peak during the bubble while oil prices have risen to over $100 per barrel again. Stocks have been reflated back to near their record high during the bubble, with the Dow Jones Industrial Average breaching the 14,000 mark last week. Real estate markets in Manhattan and Washington, D.C. are at all-time highs as are Midwestern farmland prices.

In contrast, the real economy is still stagnating, with real GDP shrinking by 0.1 percent during the fourth quarter of 2012 and the unemployment rate for January ticking up from 7.8 to 7.9 percent. No doubt aware of the tepid performance of the real economy, and its failure to respond to the policy he advocates, Sumner stakes out an odd and silly fallback position. The U.S., he argues, like Japan and Europe, has entered a stage of permanently depressed growth. As Baum reports, Sumner believes “slow nominal and real growth and ultra-low interest rates are less a temporary phenomenon than the norm in developed nations with aging populations.” The U.S. economy, Sumner says, is experiencing “long- term secular decline in real interest rates, from 7 percent to negative 1 percent now, at the same time inflation has been trending down.” In other words, low interest rates are not mainly a result of the Fed’s actual inflationary monetary policy, but of some imaginary secular stagnation that Sumner has conjured up.

There is no surer sign that market monetarism is soon destined for the dustbin of failed economic doctrines than Sumner’s resort to the long-discredited “stagnation thesis” proposed by Keynesian Alvin Hansen in the late 1930s. It is somewhat ironic that the blogonomic phenomenon of market monetarism will barely survive the publication of the first Kindle book expounding the doctrine.