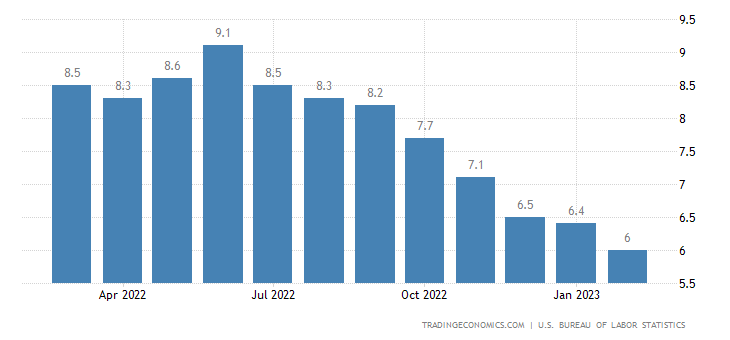

Recently, the Fed raised interest rates by 0.25 percent, after another 0.25 percent hike in February. The interest rate is now at 4.9 percent. The annual consumer price index (CPI) has been decreasing in recent months and it was 6 percent in February. However, according to Shadow Government Statistics, if we measure the CPI by the methodology used in the 1980s (see how the CPI’s methodology was changed here), the CPI has also decreased in recent months, but it is barely below 15 percent.

After the collapse of FTX and the layoffs in the tech sector in November, the US banking sector is the one bleeding right now. The US has been living in an artificially ultra-low interest rate (or negative real rates) environment since 2001. This created a lot of distortions in the allocation of resources in the economy, by incentivizing companies and financial institutions to take huge risks. Plus, bank regulations made by the US government encouraged banks (through favorable accounting) to accumulate Treasurys and mortgage-backed securities (MBSs) since they didn’t take a haircut on those assets (and neither they were required to mark them to market). So, as those assets were losing value, banks could pretend there were no losses.

The US banking system was bailed out by the Fed shortly after the collapse of Silicon Valley Bank and Signature Bank and the Fed’s balance sheet increased again (chart 1) and is now at $ 8.7 trillion (the peak was $ 8.9 trillion). The monetary base (M0) likely increased as well, but the data is not up to date.

The decrease in the CPI is mainly due to the fact that the monetary aggregates were contracting. As the Fed was no longer buying Treasurys and MBSs, the monetary base (M0) was not increasing and even underwent a small contraction since April 2022. Bear in mind that the bailout mentioned above is not yet an official quantitative easing (QE). That is, the Fed is not effectively buying banks’ assets, but rather making loans to them using these assets as collateral (however, to do so, it increases the monetary base to make these loans and puts these assets in its balance sheet; so, it’s the same effect).

Chart 1: Fed Balance Sheet (Green) and M0 (Red), 2020–23

Source: FRED; author’s own elaboration.

M1 and M2, which include money that actually circulates in the economy and which have actual influence on consumer prices, also contracted in recent months, after a significant increase in 2020-21.

Note: Murray Rothbard’s and Joseph Salerno’s true money supply (TMS) is a more precise measure of money circulating in the economy. TMS differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits and retail money funds).

If M1 and M2 increase significantly (like it did in 2020-21) alongside M0, then the CPI is likely to rise again. The increase in M0, by itself, does not cause consumer price inflation, but it does cause misallocations of resources in the economy (as the central bank buys rotten assets, preventing companies and financial institutions that are wasting resources (they make investments with no return) from going bankrupt and releasing those resources for potential sustainable investments. The expansion of M0 also causes asset price inflation (real estate, bonds and stocks).

This latest interest rate hike raised the IORB (Interest Rate on Reserve Balances), which is the main rate the Fed uses to influence the Federal Funds Rate (FFR), from 4.65 percent to 4.9 percent. In July 2021, the interest rate on reserve balances replaced the interest rate on excess reserves (the interest that banks received from the Fed on excess reserves they held with the Fed and which was the rate that the Fed used, since 2008, to influence the federal funds rate) and the interest rate on required reserves (the interest rate on reserves that banks are required to hold with the Fed). For details on how the Fed began to use the interest rate on excess reserves to influence the federal funds rate in 2008, read pages 61–68 of my article at Procesos de Mercado.

Note that the federal funds rate has been almost on the same level as the interest rate on excess reserves (and now as the interest rate on reserve balances):

Chart 2: Federal Funds Rate (Red), Interest Rate on Excess Reserves (Green), and Interest Rate on Reserve Balances (Orange), 2019–23

Source: FRED; author’s own elaboration.

The Federal Open Market Committee – FOMC stated:

The Committee anticipates that some additional [monetary] policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation [prices] to 2 percent over time.

However, it also stated:

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.

This could be seen as an indication that the Fed rate hikes may be near the end. And we can never trust the FOMC’s projections.

And the fact that the Fed is increasing its balance sheet again already undermines its commitment made at the February meeting:

[...] the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

This same commitment was made in the last meeting.

An increase in interest rates means a decrease in the prices of fixed-income assets (like corporate bonds and government bonds) and a reduction in the present value of future revenues of companies (which makes their stocks go lower). In Q4 2022, banks registered unrealized losses. The total of these unrealized losses (including securities that are available for sale or held to maturity) was about $620 billion. Unrealized losses on securities have meaningfully reduced the reported equity capital of the banking industry.

With the Fed raising rates once again, there could be more turmoil in the banking system and/or other sectors of the financial market as these losses tend to increase. The Fed is loosening monetary policy on the one hand (by expanding the M0) and tightening it on the other hand by raising rates. It makes no sense.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}